[ratings]

This article discusses the method of generating two correlated random sequences using Matlab. If you are looking for the method on generating multiple sequences of correlated random numbers, I urge you to go here.

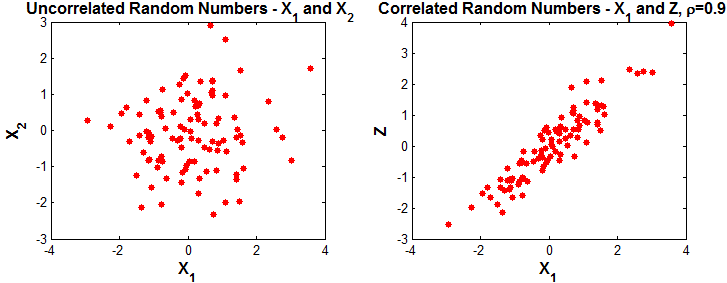

Generating two vectors of correlated random numbers, given the correlation coefficient $latex \rho$, is implemented in two steps. The first step is to generate two uncorrelated random sequences from an underlying distribution. Normally distributed random sequences are considered here.

[table id = 36/]

Step 1: Generate two uncorrelated Gaussian distributed random sequences $latex X_1, X_2$

x1=randn(1,100); %Normal random numbers sequence 1

x2=randn(1,100); %Normal random numbers sequence 2

subplot(1,2,1); plot(x1,x2,'r*');

title('Uncorrelated RVs X_1 and X_2');

xlabel('X_1'); ylabel('X_2');Step 2: Generate correlated random sequence z

In the second step, the required correlated sequence is generated as

$latex Z=\rho X_1 + \sqrt{1-\rho^2} X_2 &s=2$

rho=0.9;

z=rho*x1+sqrt(1-rhoˆ2)*x2;%transformation

subplot(1,2,2); plot(x1,z,'r*');

title(['Correlated RVs X_1 and Z , \rho=',num2str(rho)]);

xlabel('X_1'); ylabel('Z');The resulting sequence Z will have $latex \rho$ correlation with respect to $latex X_1$

Results plotted below.

Rate this article: [ratings]

Further reading

Topics in this chapter

[table id=33 /]

Books by the author

[table id=23 /]